Everything Buyers, Sellers, and Agents Need to Know:New Disclosure Form, As-Is Sales Still OK, Exemptions, and Other Changes to Current Practice

Starting October 15, 2025, Massachusetts joined a small handful of states that ban sellers and agents from forcing homebuyers to waive their right to a home inspection. The new regulation — 760 CMR 74.00 — Residential Home Inspection Waivers (PDF) — was adopted by the Department of Housing and Community Development to crack down on the increasingly common practice of pressuring buyers into waiving inspections just to “win” a bidding war.

What the New Law Says

No Forced Waivers. A seller (or their agent) cannot condition acceptance of an offer on the buyer agreeing to waive or restrict a home inspection.

No Back-Door Waivers. Sellers also cannot accept an offer if they know — directly or indirectly — that the buyer intends to waive an inspection.

Buyer’s Choice. Importantly, buyers can still decide, on their own, after signing and receiving the disclosure, to waive or limit an inspection. The difference is: sellers can’t demand it up front. An inspection waiver provision can be included in the Purchase and Sale Agreement but should be drafted carefully and should reference 760 CMR 74.00 and the fact that the buyer waives it voluntarily and willingly after receipt of the required disclosure form.

As-Is Sale Still Allowed. Sellers can still insist on an “as-is” sale provision in a purchase and sale agreement which effectively bars a buyer from making a property condition claim after the closing. Nothing in the new law requires a seller to agree to make repairs or improvements, or agree on a price reduction, based on the results of a home inspection. Of course, the parties can still negotiate and agree on these matters as we have always done.

Meaningful Inspections Only. Contract clauses that make an inspection effectively impossible — for example, giving only 24 hours to schedule one or preventing a buyer from backing out after major defects are found — are prohibited.

Who’s Covered The regulation applies to most residential real estate sales — single-families, condos, co-ops, and multi-family homes up to 4 units.

Exemptions include:

Family or related-party transfers

Foreclosures, deeds-in-lieu, and auction sales

Certain new construction sales (if the builder provides a one-year written warranty)

Why This Matters If you’ve bought or sold a home in the last few years, you know the drill: in a competitive market, listing agents would flat-out tell buyers, “If you want this property, you’ll need to waive your inspection.” That left buyers vulnerable to hidden defects — structural, environmental, or safety — with no recourse.

Now, that practice is over. Well, kind of. Sellers who ignore the law risk violating M.G.L. c. 93A (the Consumer Protection Act), exposing themselves (and their brokers) to lawsuits, triple damages, and attorney’s fees. However, the market will adapt to these new changes, and I still see buyers agreeing to waive their right to a home inspection – which they can still do so long as they sign the required disclosure form and the offer itself makes no mention of an inspection waiver.

Practical Tips

For Buyers: You don’t have to feel bullied into skipping inspections anymore. But remember: you can still waive if you truly want to — it just has to be your choice.

For Sellers/Agents: Build this new disclosure into your workflows. Do not include waiver language in Offers.

For Attorneys: Watch for boilerplate clauses in older templates that might “render the inspection meaningless.” Those will now be risky under Chapter 93A.

Bottom Line Massachusetts is taking a strong consumer-protection stance: buyers should have a fair shot at protecting themselves with an inspection. The days of “no inspection, no deal” are gone. Well, sort of…

I’ll be monitoring how this plays out in practice — especially in competitive markets like Greater Boston. If you’re a buyer, seller, or broker with questions about how the new regulation impacts your deal, feel free to reach out to me at [email protected].

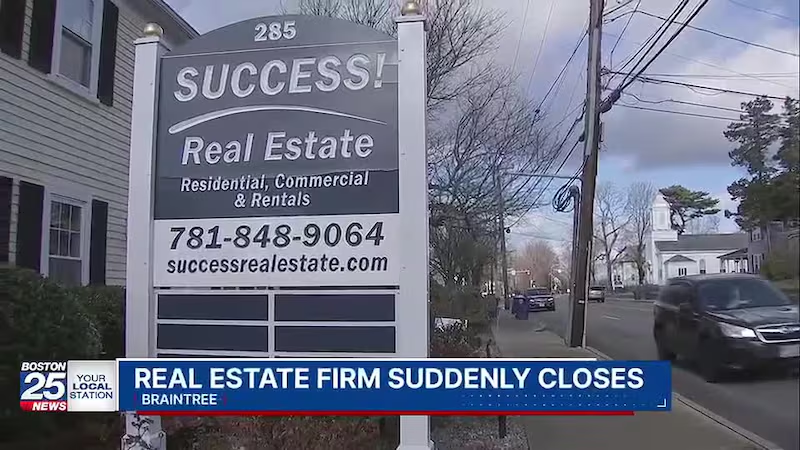

Owner Stephen Webster Accused Of Pilfering Over $1 Million In Escrow and Firm Funds

As you may have seen on Boston 25 News or read in the papers, Success Real Estate, Inc., a 140 agent real estate firm based on the South Shore, suddenly closed on December 14, 2024, surrounded by allegations that its owner, Stephen Webster embezzled over $1 Million in escrow deposits, broker commissions, and personal loans from agents. Since then, Success and Webster have been sued by over 15 agents and buyers who are scrambling to recover hundreds of thousands in unpaid commissions, deposits on pending transactions, and even personal loans given by agents to Webster in an attempt to keep the firm afloat. One of these lawsuits (embedded below) is one that I filed in Norfolk Superior Court on behalf of a top agent, where the judge granted real estate attachments against Webster and Success’ properties and assets. The Success Real Estate debacle has renewed focus on lax state regulation of broker escrow deposit accounts.

Perfect Storm of Personal Greed, Market Downturn, and Financial Mismanagement

The Success Real Estate debacle appears to have been caused by a deadly combination of financial mismanagement, the turndown in the real estate market, and the extravagant lifestyle and personal greed by Webster. The writing was on the wall when over the last year, Webster could not obtain traditional financing and was left to ask for over $300,000 in personal loans from the very agents whom he supervises. As alleged in the lawsuits, Webster fraudulently procured these loans by falsely representing to each lending party that he had the financial ability to repay the loan in full and that it would benefit them, as agents of Success. In actuality, Webster obtained these loans no different than a “Ponzi” scheme as he was simultaneously embezzling over $1 Million from Success’ coffers in order to fund business operations and jetting between Boston and his $10,000/month Florida home on the intercoastal, as claimed in the litigation. The Attorney General’s Office is now conducting an active and ongoing investigation into the matter, and I will not be surprised if and when Webster is charged with a slew of felonies.

Renewed Focus on State Oversight of Broker Escrow Accounts

One of the worst parts of this debacle is that Webster allegedly pilfered his firm’s escrow account which holds the earnest deposit funds of buyers on pending transactions. Rumors are swirling that the exposure is well over $1 Million in the escrow account alone. This is arguably the worst thing a broker could ever do because these down payment deposits are often the life savings of innocent families. So this begs the question: Where was the state Board of Registration of Real Estate Brokers and Salespersons which has oversight over broker escrow accounts? The Board is supposed to conduct periodic audits of broker escrow accounts, but based on discussions I’ve had with people with knowledge of the Board’s operations, these audits are nothing more than a 10 minute check-in and do not examine the account inflows and outflows and bank records which could spot irregularities. When was Webster’s last audit and what did it show, if anything? Furthermore, the state required bond for escrow accounts that brokers must obtain only covers $5,000 in losses, which is insane. One can easily conclude that the inadequate state oversight of Success contributed to this debacle. State legislators and regulators should take a hard look at the Board of Registration audit operations and bond amount in order to prevent something like this from happening again.

I’m sure there will be many more claims filed against Success and Webster in the near future. I will keep readers updated with any developments. If you have any information you would like to share or if you are a victim of Success and Webster and want to file a claim, please contact me at [email protected].

A Massachusetts Real Estate Litigator Talks About Lis Pendens Basics, Strategy, and Pro Tips.

Recently, I gave a well attended webinar for the Real Estate Bar Association on a subject that is near and dear to my real estate litigator’s heart — The Massachusetts Lis Pendens. The webinar was an introductory presentation which I called “Lis Pendens 101,” and covered essentially all the basics from what is a lis pendens, how to get one, how to defend against one, and everything in between. I’m basically going to convert my presentation into this blog post. I’m going to write it for both lawyers and the general public, so some of it may seem basic while other parts may seem complex. Ok, let’s do this.

What Is A Lis Pendens?

Well, let’s start with the Latin translation of the term “lis pendens.” It means “a suit pending.” Here in Massachusetts, a lis pendens is a notice of a lawsuit recorded at the registry of deeds against the title to the particular property at issue in that lawsuit. A lis pendens must be approved by a judge who must find the lawsuit “affects the title to real property or the use and occupation thereof or the buildings thereon.” Once recorded at the registry of deeds, a lis pendens can effectively stop a purchase or sale of real estate from closing, create a “cloud” on title, and otherwise prevent a party from taking adverse action involving the subject property. Additionally, title insurance companies routinely decline to insure a title with a lis pendens on title. The lis pendens really earns its well-deserved reputation as deadly arrow in a real estate litigator’s quiver.

For Which Type of Case Can You Get a Lis Pendens Issued?

The lis pendens procedure is governed by statute, Mass. Gen. Laws ch. 184, sec. 15, and practitioners should be intimately familiar with it. The statutory standard for obtaining a lis pendens is that the lawsuit “affects the title to real property or the use and occupation thereof or the buildings thereon.” Ok, so what does that mean? Some examples of cases that are covered are:

Real Estate Contract Disputes/Specific Performance

Boundary Line/Easement Disputes and Adverse Possession

Quiet Title Actions

Restrictive Covenants

Please note that under the statute, in Zoning/Wetlands Appeals cases, you are not entitled to a lis pendens — this was enacted to keep real estate development permitting from being railroaded by abutter appeals.

How To Get a Lis Pendens

First off, you need an experienced real estate litigation attorney because the process is complicated. The attorney will draft a Verified Complaint which must be signed by the plaintiff client under the pains and penalties of perjury attesting that all facts are true and accurate, and no material facts have been omitted. The “no material facts have been omitted” requirement was added in 2002, and I’ll discuss this below as there has been recent case law on it. The complaint must name as defendants all owners of record and any party in occupation under a written lease. Along with the Verified Complaint, the attorney will file a Motion for Issuance of Lis Pendens, a proposed Memorandum of Lis Pendens, and Motion for Short Order of Notice.

You also have to pick your venue, which is between Superior Court and Land Court. There are a lot of factors which will go into that calculation, including how complex your case is, whether you want a jury trial, and whether you want your case in Boston (Land Court).

The way I handle a lis pendens is that I will file the case in person in the afternoon and seek what’s called a “short order of notice,” which accelerates the time schedule for getting the motion for lis pendens heard by the judge. You get to pick a hearing “return date” and then you must serve a Summons and Order of Notice along with all the other pleadings on the defendant(s) by sheriff or constable. Then you wait a couple weeks until the hearing date and any opposition or special motion to dismiss from the opposing side (which I’ll cover below). If there is a clear danger that the other party will convey or encumber the subject property, you can file the motion “ex parte” – that is, without the other side being notified in advance, however, you have to make that factual showing there is an emergency.

At the hearing on the motion for lis pendens, both sides and their attorneys will argue before the judge whether the case qualifies for the issuance of a lis pendens. In theory, the standard for getting a lis pendens is quite low. There should not be any debate over the merits of the claims; the only issue is whether the case qualifies for a lis pendens. However in practice, especially if the defendants are opposing the lis pendens or have filed a special motion to dismiss, you’ll get deep into the merits of the case at that hearing.

Defending The Lis Pendens

With the 2002 amendments to the lis pendens statute, there are now several ways to attack a motion for lis pendens. When I was first practicing back in the late 1990’s, judges would give out lis pendens like candy. Not anymore.

A party defending a lis pendens may now file a “special motion to dismiss.” If a judge allows the special motion to dismiss, any claim affecting title will be dismissed AND the plaintiff will have to pay the defense’s attorney’ fees and costs. Additionally, the case is basically frozen in place until the special motion is ruled upon. So this remedy has a lot of teeth. However, getting a judge to grant a special motion to dismiss is not easy. You must demonstrate that the action is frivolous because (1) it is devoid of any reasonable factual support; or (2) it is devoid of any arguable basis in law; or (3) the action or claim is subject to dismissal based on a valid legal defense such as the statute of frauds. In my 25 years, I’ve only had a handful of cases thrown out on a special motion to dismiss.

Another way to attack a motion for lis pendens is to focus on what may have been left out of the plaintiff’s lawsuit. Under recent case law, a party’s failure to include all material facts in its complaint or required certification may result in denial of lis pendens and dismissal of that party’s claims where the omitted facts establish that those claims are devoid of reasonable factual support or arguable basis in law. Some cases detailing this strategy are: McMann v. McGowan, 71 Mass. App. Ct. 513 (2008); Galipault v. Wash Rock Invs., LLC, 65 Mass. App. Ct. 73 (2005); DeCroteau v. DeCroteau, 90 Mass. App. Ct. 903 (2016). I’ve used this strategy several times successfully resulting in the judge declining to issue a lis pendens where the plaintiff left out critical facts in his complaint.

The Memorandum of Lis Pendens

If you have the good fortune of convincing the judge to issue a lis pendens in your case, your attorney will have the judge endorse a Memorandum of Lis Pendens form which then is recorded at the registry of deeds. The Memorandum must contain the caption of the case, the record owners, address, and deed reference to the subject along with the judge’s endorsement that: “It is hereby found and ordered that the subject matter of this action constitutes a claim of a right to title to real property or the use and occupation thereof or the buildings thereon within the statutory definition of G.L. c. 184, § 15.” A certified copy of the Memorandum of Lis Pendens along with Affidavit of Service (service by certified mail) must be recorded either in person or through the e-record system.

The lis pendens stays on record (and creating a cloud on title) during the entire pendency of the case, which can go on for many years. That’s what makes it so powerful, and in many cases, can force a party into a favorable settlement or resolution.

Appeals

Ok, you’ve either got your lis pendens or you may have lost and had a lis pendens issued against you. Can I appeal? The answer is maybe, and it’s complicated. An “interlocutory appeal” is available to a Single Justice of the Appeals Court available under G.L. c. 231, s. 118, first and second paragraphs for “any party aggrieved by a ruling [under the statute].” A full panel appeal to the entire Appeals Court is also available. There is a hard 30 day appeal period for both. An appeal covers the denial/grant of lis pendens and a grant of a special motion to dismiss, but not the denial of a special motion to dismiss. Practicioners should review the statute carefully and DeLucia v. Kfoury, 93 Mass. App. Ct. 166 (2018); Citadel Realty LLC v. Endeavor Capital North, 93 Mass. App. Ct. 39 (2018). The best practice is to file single justice appeal and notice of appeal in lower court for full panel appeal.

Dissolution

Once a lis pendens goes on record, it doesn’t go away unless it is properly dissolved. If the parties are fortunate enough to settle the case, dissolving the lis pendens is fairly easy with the attorneys signing and recording a formal Dissolution of Lis Pendens, or a Stipulation of Dismissal, then certified copy of Judgment of Dismissal. If you get the lis pendens dissolved by the court or even better, the entire case dismissed prior to judgment, you’ll need to record certified copy of Order Dissolving Lis Pendens and/or Certificate of Judgment.

___________________________________

I often refer to the lis pendens as a real estate litigator’s best friend and worst enemy. It can make the difference between winning and losing your real estate case, and most often creates the leverage needed to secure a favorable resolution. If you have any questions regarding the lis pendens process, feel free to email me at [email protected].

The Difference Between Winning and Losing A Real Estate Contract Lawsuit

I have handled countless cases enforcing and defending real estate contracts, particularly involving Offers to Purchase and Purchase and Sale Agreements. For buyers, these cases typically involve the standard form Offer (or Contract) to Purchase, a one or two page short form contract, which under Massachusetts law (McCarthy v. Tobin) is a binding and enforceable contract. The seller then usually attempts to wriggle out of the deal or may even receive a higher or better offer. Sometimes the transaction has progressed past the execution of the Purchase and Sale Agreement and falls apart, and the buyer still wants to close, or the seller believes the buyer has violated the agreement and wants to retain the buyer’s deposits. When that occurs, litigation often ensues.

Specific Performance

The buyer wants to pursue the deal, and asks “Can a judge make the seller perform and close?” The answer is yes, under the theory of “specific performance.” However, the buyer must establish several elements for such a claim. The buyer must establish: (1) the existence of a written contract containing reasonably specific terms signed by or duly authorized by the other party and otherwise binding upon such party, and (2) the breach of that contract by the seller. The breach of contract may be shown by (i) a clear repudiation of the contract by the seller, (ii) the buyer’s tender of performance, formally or by notice, and (iii) a demand for performance with the buyer ready, willing, and able to proceed to a closing.

A solid paper trail is critical to winning these cases. The parties and their transactional lawyers in the underlying deal should always document the seller’s repudiation or breach of contract and the buyer’s willingness to close, preferably by letter or email. These days, text messages can also be helpful, but often open to differing interpretations. Armed with exhibits of emails and texts, the buyer’s attorney can often persuade the judge that the seller has unjustifiably breached the contract and issue a lis pendens (discussed below), and after trial or summary judgment, an award of specific performance.

Obtaining Leverage — The Lis Pendens

The difference between winning and losing (or settling favorably) is for the buyer to obtain a Lis Pendens from the court. As I have written about in this article, a lis pendens is Latin for “a suit pending.” The lis pendens is recorded at the registry of deeds against the property and its owner(s), creating a cloud on the title to the affected property. A lis pendens will, in many cases, effectively prevent the owner from selling the property while the lawsuit is pending — which could be years, thereby giving a buyer incredible leverage in the case. In order to obtain a Lis Pendens, a buyer must show that the claim “affects the title to real property or the use and occupation thereof or the buildings thereon.” A buyer should file a motion for lis pendens right from the start of the case, seeking a quick hearing on the motion, or even ex parte (without the seller getting advance notice, if there is a clear danger that the property will be conveyed).

Defending the Lis Pendens and Claim for Specific Performance

If you are a seller defending a claim for specific performance and a motion for lis pendens, the deck is often stacked against you out of the starting gate. The standard of review favors the buyer because unlike obtaining an attachment or other pre-judgment lien, a lis pendens does not require a showing a likelihood of success on the claim. A lower standard is used — the claim must not be frivolous or lack an arguable basis in fact or law. Further, buyers typically run into court quickly, and there is often a time crunch to gather and marshal all the evidence before the initial hearing on the motion for lis pendens. Nevertheless, I have been successful in beating back lis pendens motions by raising defenses such as the Statute of Frauds, which requires a writing signed by the party to be charged, and other contractual defenses.

Special Motion to Dismiss and Certification That No Material Facts Have Been Omitted

In defending claims for specific performance and lis pendens’, I have been most successful using the “special motion to dismiss” and raising the requirement that plaintiffs must certify that no material facts have been omitted from their complaint.

The “special motion to dismiss” is a newer tool which allows defending parties to dismiss a lawsuit seeking a lis pendens by showing: that the action or claim is frivolous because (1) it is devoid of any reasonable factual support; or (2) it is devoid of any arguable basis in law; or (3) the action or claim is subject to dismissal based on a valid legal defense such as the statute of frauds. This standard is relatively high, however, it can be reached with the right factual record and defenses in play.

I’ve also had success pushing another one of the new requirements of the amended Lis Pendens Statute: the requirement of a verification on a complaint to “include a certification by the complainant made under the penalties of perjury that . . . that no material facts have been omitted therefrom.” Courts have ruled that a party’s failure to include all material facts in its complaint may result in the dismissal of that party’s claims where the omitted facts establish that those claims are devoid of reasonable factual support or arguable basis in law. If the plaintiff has failed to disclose all of the relevant facts in the case, often those which are unfavorable, you can raise this defense which may give you some traction with the judge.

As you can see, this area of law is quite complex for the layperson. Consultation with an experienced real estate litigator is paramount. If you are dealing with such a case, feel free to reach out to me at [email protected].

Update: 4/22/20 — The Senate has passed a new revised version of the Bill, now it moves on to the House where it is expected to pass.

The real estate legal community, including yours truly, have been working and lobbying tirelessly to address the various impacts of the Coronavirus (COVID-19) Crisis on real estate transactions and closings. One of the first solutions we proposed is legislation allowing for remote or virtual notarizations of deeds, mortgages and other closing documents so that buyers and sellers can sign documents in the safety of their own homes on their computers. Due to the COVID-19 crisis, many folks are subject to the Governor’s Stay At Home Order or don’t feel safe traveling outside to an attorneys’ office for a real estate closing. Meanwhile, while the economy heads towards a recession, real estate is one of the few assets with available equity for consumers.

Under our proposed legislation, An Act Relative To Remote Notarization During COVID-19 State of Emergency (S.D. 2882), a licensed Massachusetts attorney may notarize legal documents using video-conferencing technology. There is a two-step process laid out in the legislation to complete the notarization process where the signer shows the attorney his/her state issued identification, sends the original signed documents back to the attorney, and then verifies the authenticity of the signed documents. Once that process is complete, the attorney can stamp the documents as notarized and must also complete and sign an affidavit attesting that all requirements have been met. Those notarized documents may then be recorded with the Registry of Deeds as valid, legal and binding recordable instruments. Additionally, the two video-conferences must be recorded and kept on file for 10 years. The bill would only be in effect during the COVID-19 State of Emergency.

The bill has widespread industry support from the Real Estate Bar Association (including the Probate Section), the Massachusetts Bar Association, the Massachusetts Association of Realtors and Greater Boston Real Estate Board. Twenty three (23) states have now passed remote notarization bills, including just recently due to the COVID19 crisis, including New York State, Vermont, Connecticut, Florida, Virginia, Texas, and Nevada. Moreover, a nationwide bill has been proposed by the American Land Title Association.

There are a number of technology companies that offer end-to-end remote notarization systems and are approved by national title insurance companies and lenders. They include:

To our real estate partners and colleagues, WE NEED YOUR HELP NOW! We need you to email or call your State Rep. and Senator and tell them you support our proposed legislation, An Act Relative To Remote Notarization During COVID-19 State of Emergency (S.D. 2882). To search for your state legislator, please click here.

Thank you! I will keep you posted as to developments and hopefully passage of the bill. Also many thanks to Attorneys Kosta and Nik Ligris on spearheading the bill!

Closings May Proceed Forward Without Smoke Detector Inspection Certifications

Due to the Coronavirus Crisis, many local fire departments have been ceasing state mandated smoke detector inspections, which are required for real estate transactions to close. I’m happy to report that on March 20, 2020, after intense lobbying from the real estate industry, Gov. Baker issued an Emergency Order allowing for the deferral of inspections by local fire departments until the Coronavirus (COVID-19) State of Emergency is lifted. The Order is embedded below and can be found here: COVID-19 Order Permitting the Temporary Conditional Deferral of Certain Inspections of Residential Real Estate.

Inspections may be deferred only if the following requirements have been met:

The parties agree in writing that the buyer, not the seller, shall be responsible for installing approved smoke/CO detectors in the premises;

The buyer agrees as a condition of taking title to equip the premises with approved detectors immediately after the closing

The state required smoke/CO detector inspection must be conducted no less than 90 days after the Mass. COVID-19 State of Emergency is lifted.

We (real estate attorneys) are drafting up new compliance agreements and language for Offers and Purchase and Sale Agreement to comply with this new Order. Please email me at [email protected] for assistance.

SignificantImpacts Hitting: Registry and Court Closures, Closing and Financing Delays, Social Distancing,School Closings, Quarantine Potential

As I was writing this post tonight, Gov. Baker ordered the shutdown of all schools through April 6, closed down restaurants and bars, and is banning gatherings over 25 people. Also announced tonight is the shut down of all Trial Court facilities on March 16 and March 17, which includes the Cambridge and Suffolk (Boston) Registries of Deeds. We are now hitting the tipping point, and going forward there will be substantialimpacts on the real estate and legal industry.

I first wrote about the Coronavirus (COVID-19) global pandemic five days ago. Seems like an eternity ago. As of that writing (data as of March 9), there were 729 reported cases in the US, with 27 deaths. As of tonight March 15, cases have over quintupled with Johns Hopkins reporting 3,722 confirmed cases and 61 deaths. With the well publicized testing delays, the real number of cases are likely far higher.

Registry of Deeds Impacts

As mentioned above, Gov. Baker just ordered the closure of all Trial Court facilities for Monday March 16 and Tuesday March 17. Both Cambridge and Suffolk (Boston) Registries are housed in Trial Court facilities so they will be closed for those two days. I spoke to Maria Curtatone, Registrar of Deeds for Cambridge Middlesex South, and she indicated that this may well be the precursor to widespread shutdown of all registries of deeds and courts throughout the state. We will await further announcements on that.

Update (3/17/20)— Suffolk and Cambridge are closed to the public until at least April 6. Currently, they are both still processing electronic recordings for recorded land. All Land Court recordings and plans must be sent in by overnight or regular mail.

We have just received a chart below showing current Registry status:

I remain concerned, however, that all Registries will be forced to shut down and will not offer in person, mail or electronic recordings. If that occurs, we will see a potentially catastrophic impact to real estate in Massachusetts. Title insurance companies have assured its attorney agents that they will offer “gap coverage” in case recordings are delayed. This coverage offers insurance coverage between the time of the physical closing and the time of actual recording of documents at the registry. However, it remains to be seen how this will play out. Will mortgage payoffs still be processed even though deeds will not be recorded? Will sellers allow buyers to get keys and move into homes if deeds aren’t recorded and their sale proceeds are held in escrow? We will need to work through these issues.

I am also concerned if COVID-19 starts hitting closing attorney offices. If a lawyer or staff member is infected, it could result in the quarantine of their entire office, essentially shutting it down for some time.

COVID-19 Contingency Provision

In my previous post, I discussed a new COVID-19 Impact Clause for Offers Purchase and Sale Agreements. (Sample language below). It is imperative that these clauses are used in both Offers and PSA’s. It’s also very important that all parties and their attorneys work together cooperatively throughout this crisis, acknowledging that there will likely be substantial impacts and delays. The goal, as always, is to get to the closing and complete the deal, by any means necessary.

COVID-19 Impact Provision. The Time for Performance may be extended by either Party by written notice for an Excused Delay which materially affects the Party’s ability to close or obtain financing. As used herein an Excused Delay shall mean a delay caused by an Act of God, declared state of emergency or public health emergency, pandemic (specifically including Covid-19), government mandated quarantine, war, acts of terrorism, and/or order of government or civil or military authorities. Notwithstanding anything to the contrary contained in this Agreement, if the Time for Performance is extended, and if BUYER’S mortgage commitment or rate lock would expire prior to the expiration of said extension, then such extension shall continue, at BUYER’S option, only until the date of expiration of BUYER’S mortgage commitment or rate lock. BUYER may elect, at its sole option, to obtain an extension of its mortgage commitment or rate lock. Notwithstanding the foregoing, said Extension shall not exceed [insert number of days].

Virtual and Remote Closings

Another impact that we are already seeing is that parties to the real estate transaction are afraid of traveling outside their homes right now (or even being visited at home) and being in contact with other people, especially those who are high risk. My colleagues and I are working on an emergency executive order for Gov. Baker to sign which would temporarily authorize remote or virtual closings using such technology as Zoom and Docusign.

Update (3/17/20): The Supreme Judicial Court today ordered that, because of the public health emergency arising from the COVID-19 pandemic, beginning tomorrow (March 18, 2020) and until at least April 6, 2020, the only matters that will be heard in-person in Massachusetts state courthouses are emergency matters that cannot be held by videoconference or telephone. Each of the seven Trial Court departments, in new standing orders to be issued today, will define emergency matters for their departments. As a result of the SJC order, courthouses will be closed to the public except to conduct emergency hearings that cannot be resolved through a videoconference or telephonic hearing. Clerk’s offices shall remain open to the public to accept pleadings and other documents in emergency matters only. All trials in both criminal and civil cases scheduled to commence in Massachusetts state courts between today and April 17, 2020, are continued to a date no earlier than April 21, 2020, unless the trial is a civil case where the parties and the court agree that the case can be decided without the need for in-person appearance in court. Where a jury trial has commenced, the trial will end based on the manifest necessity arising from the pandemic and a new trial may commence after the public health emergency ends. Courts, to the best of their ability, will attempt to address matters that can be resolved or advanced without in-person proceedings through communication by telephone, videoconferencing, email, or other comparable means.

In addition to the closings on March 16-17, the Massachusetts Court System announced over the weekend major “triage” changes reducing the number of persons entering state courthouses. These rules are effective Wednesday March 18, 2020. A link to all of the new changes can be found here — Court System Response to COVID-19. A summary of each court and respective changes are as follows:

Superior Court — All jury trials postponed until April 22. Motions handled by individual judges with preference for telephonic hearing and postponement where necessary to limit number of people entering courtroom. Emergency matters may proceed normally. The new Standing Order 2-20 can be found here.

Housing Court — All cases including evictions (except emergencies) postponed until after April 22. Matters may be heard earlier upon a showing of good cause. New Housing Court Standing Order is here.

Probate and Family Court — Trials postponed until May 1. Motions and pre-trials heard telephonically or postponed until after May 1. Modification complaints won’t be heard until after May 1. New Probate and Family Court Standing Order 1-20 is here.

District Court — No jury trials until after April 21. All criminal appearances rescheduled for 60 days, and no earlier than May 4. Arraignments and Bench trials may proceed. The new District Court Standing Order is here.

Land Court — All trials postponed until after April 21. All other motions and proceedings shall be held telephonically at judge’s discretion. Registration of title documents should not be done in person. Mail or email is now preferred. (Not sure how that will work). New Land Court Standing Order 2-20 is here.

Appeals Court — Oral argument for March will be telephonic.

Supreme Judicial Court — Please see the Court’s website.

As you can glean from the changes, virtually all trials are being pushed out through the end of April. Motion hearings are court specific with telephonic hearings being substituted for in-person hearings. Of course, if the courts are all shut down, all bets are off. With no staff, the courts will not even be able to handle new filings. The system would just stop in its tracks, except for the most emergency of matters.

Lender/Financing Delays

This week we will see if there are any major disruptions to lenders’ ability to provide financing. I am seeing some smaller mortgage companies moving to remote employee staffing. I’m also hearing about appraisal delays. If there are government employee impacts such as at the IRS for processing tax transcripts, there could be delays with underwriting. I think it’s inevitable that we will be seeing lender delays moving forward.

Municipal Closings

I am also hearing of closings of municipal departments, which may affect the availability of final water/sewer readings and possibly smoke detector certificates. Title 5 inspections could also be impacted.

25 Person Social Gathering Restriction

New restrictions on crowd sizes that Gov. Charlie Baker issued on Sunday, March 15, could upend open houses. The restrictions banned gatherings of 25 or more people. Brokers seemed to anticipate a possible drop-off in attendance, even before Baker’s restrictions and despite strong numbers the past couple of weeks. “Next week may be a different story,” Jason Gell, a Keller Williams broker and president of the Greater Boston Association of Realtors, said on March 12. “Unfortunately, any decline in open houses or listings is likely to make the conditions for buyers even more difficult.”

Social Distancing, School Closures and Possible Lockdown

The impacts of COVID-19 are manifesting not necessarily in the actual infection and sickness of patients (which I’m not discounting at all) but all the measures we are taking to “flatten the curve.” I want to urge all my readers that COVID-19 could wind up being the worst global pandemic since the Spanish Flu and should be taken as seriously as life and death. If you can work from home, do that and don’t go into the office. If you can arrange for remote employee access, please do that. Take advantage of technologies like Zoom, Docusign and Dotloop. Please keep your kids at home. No playdates, family gatherings or hang-outs. They say we are only 2 weeks behind Italy and you see what’s going on there. Stay safe! More updates to follow as I get them.

PotentialImpacts: Registry of Deeds Closings, Financing Delays, New Covid-19 PSA Clause, Housing Market Slow Down?

The Coronavirus (COVID-19) is a highly infectious respiratory virus, which originated in Wuhan, China, and has spread across the globe, wreaking havoc on financial markets, public health systems, schools, universities, and daily lives. As of March 9, there are 729 reported cases in the US, with 27 deaths. Here in Massachusetts, as of March 9, there are 41 cases with no reported deaths. Infectious disease experts predict that the virus will continue spreading across the United States, affecting just about every aspect of our lives.

Here in Massachusetts, we are beginning to see significant impacts. Harvard University just cancelled all classes in favor of online instructions. Mayor Walsh has cancelled the St. Patrick’s Day parade. Some schools are closing temporarily and cancelling events. Companies are cancelling conferences and restricting travel. And of course, the stock market has dropped precipitously.

Likewise, in the real estate industry we are starting to see impacts as well. Despite the COVID fear factor, most agents are still reporting robust attendance at open houses and market activity, as confirmed by Curbed Boston. However, that may soon change as the virus gets increasingly widespread and the impacts to the financial markets begin to set in. I’m going to outline some potential impacts going forward, and I’ll update this post as developments emerge.

Registry of Deeds and Court Closings

Update (3/13/20): Suffolk and Salem Registry have shut down public closings. Only title examiners and attorneys are allowed access. They are still recording documents.

We are starting to see court and government building closings in other states. Federal courts in New York’s Southern District, including Manhattan, are restricting entry. No one will be allowed in who traveled within the past 14 days to China, South Korea, Japan, Italy or Iran, or who had close contact with someone who has. Trials have been postponed in Seattle and Tacoma courts.

No closings have been announced here in Massachusetts, but it’s a possibility. Virus impacts may result in Registries of Deeds and the Land Court being forced to closed or operate with a skeleton staff.

Fortunately, we have electronic recording capabilities here in Massachusetts. If the registries are closed, hopefully they will still allow for e-recording which should enable closings to keep on track. However, registry staff must still examine each electronically recorded document so there still could be impacts. We don’t know the fully extent of the impacts, if any.

Lender/Financing Delays

I have not yet heard of any major disruptions to lenders’ ability to provide financing. However, it’s not out of the realm of reason if companies are requiring their employees to work from home, etc. Further, if there are government employee impacts such as at the IRS for processing tax transcripts, there could be delays with underwriting. The same is true if appraisers cannot get out into the field and do their reports. I’ve already heard of at least one lender asking an attorney for a COVID-19 delay provision in a purchase and sale agreement, which brings me to the next topic…

COVID-19 Delay Clause In Purchase and Sales Agreement

Due to the various impacts and possibilities for delays as outlined above, we are already seeing requests for language dealing with the Coronavirus in purchase and sales agreements. As just mentioned, there may be lender delays affecting a buyer’s ability to obtain timely financing due to virus impacts. Buyers and sellers may be subject to quarantines, or if they are traveling, they may be stuck in a public health purgatory like the Princess Cruise ship. If Registries are closed and no e-recording is allowed, then closings will need to be cancelled or rescheduled. My colleagues and I are working on a new COVID-19 clause that will balance all of these concerns.

Our draft provision (subject to change) is as follows:

COVID-19 Impacts. The Time for Performance may be extended by either Party by written notice for an Excused Delay which materially affects the Party’s ability to close or obtain financing. As used herein an Excused Delay shall mean a delay caused by an Act of God, declared state of emergency or public health emergency, pandemic (specifically including Covid-19), government mandated quarantine, war, acts of terrorism, and/or order of government or civil or military authorities. Notwithstanding anything to the contrary contained in this Agreement, if the Time for Performance is extended, and if BUYER’S mortgage commitment or rate lock would expire prior to the expiration of said extension, then such extension shall continue, at BUYER’S option, only until the date of expiration of BUYER’S mortgage commitment or rate lock. BUYER may elect, at its sole option, to obtain an extension of its mortgage commitment or rate lock. Notwithstanding the foregoing, said Extension shall not exceed [insert number of days].

Impact On The Real Estate Market

If you’re in the market for a house, all this uncertainty might have you worried about the housing market. Will it suffer a swoon similar to Wall Street? There are a few ways the virus could affect the housing market that you should be aware of. However, I think we can breath a sigh of relief, because a housing catastrophe on the scale of the 2008 financial crisis is almost certainly not going to happen.

The good news is that mortgage interest rates are still at historic lows. However, I’m also hearing that a lot of lenders are at full capacity with demand for both refinances and purchases so rates may be heading up in the very near future.

I think as we are heading towards a global recession and the continuing daily life impacts of the virus, we are going to see a slowing down of the real estate market in general. Uncertainty is the hobgoblin of the home buyer. Indeed, this is exactly what Lawrence Yun, Chief Economist at the National Assoc. of Realtors is saying:

I hope I’m wrong. Comment below or shoot me a line ([email protected]) and tell me what you’re seeing out there. I’ll keep you posted with any developments.

Allen Seymour – Arraignment Brookline District Court

Summary Judgment Ruling In Favor of Forgery Victim Allows Case to Proceed to Trial

As I’ve written here, I have been representing three victims in a brazen and complex real estate forgery scam. The ringleader was Allen Seymour of Oxford, who used forged deeds, fake notary stamps and driver’s licenses to sell properties out from under homeowners, flipping their properties to wealthy investors, and pocketing the cash. Seymour targeted properties in Cambridge, Brookline, and Somerville. By accounts, he made off with over $2M in illicit sale proceeds. Seymour also worked with a group of accomplices including a Newton police lieutenant. The cases have been featured in several Fox News 25 segments. While Seymour remains in jail awaiting trial on 22 felony indictments, the civil cases have been ongoing for almost two years, and are heading towards trial.

I just received the first major court ruling in the cases from Superior Court Justice Douglas Wilkins. The ruling is noteworthy because it appears to be the first time a Massachusetts judge has issued a written decision dealing with the unique type of forgery that occurred in this case.

The Deed Forgery Scam

Forged Deed First Page

Forged Deed Second Page

The facts of the case are pretty surreal. My client is the owner of a three family property in Brookline, assessed at $1.5 Million. He was behind on his mortgage, and Seymour (using the alias “Rich Chase”) approached him with a foreclosure rescue scheme. Seymour had him sign a mortgage payoff authorization form which contained a separate signature page with a notary block – which would be used later to perpetrate the fraudulent scam. Ordinarily, mortgage payoff authorizations are not notarized. Behind my client’s back, Seymour took the notarized signature page of the payoff form and attached it to a quitclaim deed and recorded it with the registry of deeds. This deed “sold” the property from my client to Seymour’s accomplice for some 30% of its value, at $480,000. While this was happening, Seymour orchestrated a flip of the property for $750,000 to an LLC owned by Fred Starikov, the owner of City Realty in Boston. Starikov’s LLC then took out a $850,000 mortgage on the property from Bee Investments LLC. Seymour then made off with the sale proceeds, and tried to flee the country with a duffle bag of cash and a trash bag filled with Oxycontin. Fortunately, he was caught in South Carolina by the FBI, and brought back to Massachusetts to face multiple felony charges.

Lawsuit Asserts Claims for Forgery and Fraud

On behalf of the victim, I brought claims for quiet title and fraud, asserting that the quitclaim deed was a forgery. Under Massachusetts law, a forgery of a deed conveys no title. It is null and void, and title reverts back to the original owner as if the forgery never occurred. This is very important in these cases, because a forgery would also avoid the defense asserted by Starikov and his lender being a “bona fide good faith” purchase or lender. This defense, if successful, could allow them to keep title to the property. Starikov and his lender also asserted a claim for “equitable subrogation.” This theory is used to enable a lender to seek repayment of monies paid out in the transaction (typically mortgage proceeds) on the theory of unjust enrichment and mistake.

What is a Forgery?

Starikov and his lender filed a motion for summary judgment to dismiss the case prior to trial, arguing that the deed wasn’t a forgery because my client’s signature was “genuine” and on the deed itself, and asserting the good faith and equitable subrogation defenses. In what appears to be a case of first impression, Justice Wilkins held that the transfer of an altered signature page onto a deed was in fact a forgery under the common law definition. As he wrote in his decision:

Red Flags: Good Faith and Equitable Subrogation

Judge Wilkins also rejected the good faith purchaser and equitable subrogation defenses. As I argued, the judge recognized that there were several “red flags” with the deed and the purchase and sale agreement (which was also forged) which could have put a closing attorney on notice of the irregularities in the transaction. These red flags are properly considered at trial, the judge ruled.

What’s Next?

Overall, I’m very pleased with Judge Wilkin’s ruling. He understood the issues, and provided some much needed justice for my client. So now the case will proceed to trial (or settlement). I will keep you appraised of any further developments. I’ve embedded the entire opinion below for your reading pleasure.

Parties Who Negotiated Past Purchase and Sale Agreement Deadline Waived It, Court Rules

The Massachusetts Appeals Court just came down with a ruling which should be a cautionary tale to everyone in the residential real estate business. It’s an interesting fact pattern, but not necessarily unusual. For those with short attention spans, the Court held that the standard deadline to execute the purchase and sale agreement is not necessarily a hard deadline. Rather, the deadline can be waived by the parties if they negotiate beyond the date, even without a formal extension in place. The Court also held that where the property is owned by several individuals, even if only one of those individuals sign the offer, this is not necessarily fatal to the deal.

In the case, the buyer, David Ferguson, and the seller, Joyce Maxim, signed the standard form Offer to Purchase put out by the Massachusetts Association of Realtors for the sale of residential property in Leominster. (For my post comparing the MAR form with the Greater Boston Real Estate Board, click here). It turns out that title to the property was actually held by a group of five individuals including Maxim, but we will get to that in a few. As is standard, the Offer provided that the parties would enter into a standard form purchase and sale agreement by a specific deadline. However, the seller’s attorney did not sent out a draft PSA until after the deadline, and negotiations continued well past the deadline without any issue raised by the parties or their attorneys. Both attorneys had suggested formalizing an extension of the PSA deadline at various times, but a formal extension agreement was never signed. At some point the seller’s attorney tried to cease the negotiations acknowledging that “we are well beyond our [PSA] date.” A week later, the buyer’s attorney tried to resurrect negotiations and save the deal. Further negotiations ensued between the parties, but they were abruptly stopped by the seller’s attorney who stated that the deal was for all intents and purposes dead.

Mr. Ferguson, the buyer, was naturally upset, and sued, seeking an order of “specific performance” to enforce the deal, based on well established law that an offer to purchase is a legally binding contract for the sale of real estate. (Read the case if you want to learn about various procedural issues that arose in the case with respect to the buyer’s obtaining a lis pendens and the seller’s special motion to dismiss under the lis pendens law.).

Two Important Take-Aways

The important take-aways from the ruling were twofold. First, the Court ruled that the typical deadline to execute the purchase and sale agreement is not always a hard deadline. Some people may be surprised to here that, but under Massachusetts law, a deadline in any contract can be “waived” by the parties words, actions, or conduct. Here, the Court said that a waiver of the deadline could be found where the seller’s attorney didn’t provide the draft PSA until after the deadline and the parties freely negotiated well past the deadline, even without a formal extension in place. Second, the Court also held that where the property is owned by several individuals, only having one of those individuals sign the offer is not necessarily fatal to the deal. If there is evidence that the signatory had apparently authority to sign for the others, or that the sellers ratified the offer, then the contract could be enforced. So now the buyer’s case will continue on for trial. Interestingly, during the pendency of the case, the sellers sold the property to another party. If the buyer is successfully, that new buyer is going to be very unhappy because his transfer will be voided! He may want to lawyer up himself.

Let’s Play Monday Morning Quarterback!

Now, what could have been done differently in this case to avoid the bad result for the seller? For starters, the seller’s attorney should have delivered the draft PSA on time. Once the parties started negotiations after the PSA deadline, they were in “no man’s zone” and that can only come back to hurt the sellers. Deadlines need to be taken very seriously, and sharp lawyers will always send out emails or other written reminders of them, and reserve their rights to terminate an agreement if the parties blow past a deadline without a written extension in place. The buyer’s attorney played this correctly, and didn’t push on the deadline issue because the law would favor his client on the waiver issue (which it ultimately did).

Text Messages Enforceable As Written Contract, Court Rules

With the proliferation of email and texts as the primary method of communications in real estate negotiations, it was just a matter of time before Massachusetts courts were faced with the question of whether and to what extent e-mails and texts can constitute a binding and enforceable agreement to purchase and sell real estate. In a ground-breaking case, Land Court Justice Robert Foster ruled in a case of first impression that text messages may form a binding contract in real estate negotiations–even where a formal offer has not been signed by the seller. This is huge wake up call for the remaining industry people who still believe that electronic communications are not legally binding.

St. John’s Holdings LLC v. Two Electronics, LLC

The case (embedded below) involves a commercial real estate deal between two businesses both represented by commercial real estate brokers for the purchase and sale of an industrial park property in Danvers. Two Electronics, as seller, and St. John’s Holdings, as buyer, negotiated for several weeks exchanging two “Binding Letters of Intent” spelling out all material terms of the proposed purchase of $3.2 Million. Towards the culmination of the negotiations, the real estate brokers exchanged several emails and texts, with the seller’s agent sending an email that his client was “ready to do this,” then a text that —

“[the seller] wants you to sign first, with a check, and then he will sign. Normally, the seller signs last or second. Not trying to be stupid or to the contrary, but that’s the way it normally works. Can Rick sign today and get it to me today? Tim”

The buyer signed four copies of the final Letter of Intent and tendered the deposit check with the buyer broker, after which the buyer’s broker sent the seller’s agent another text — “Tim I have the signed LOI and check. It’s 424 [PM]. Where can I meet you?” Shortly thereafter, the two agents met, and the buyer’s broker tendered the buyer signed Letter of Intent along with the deposit check.

Unbeknownst to the buyer, that same day, the seller had received another offer on the property, and proceeded to sign that offer. The seller then refused to sign the Letter of Intent with St. John’s. St. John’s sued, claiming that the series of letters of intent, emails and text messages constituted a binding and enforceable contract.

Intersection of 17th Century Statute of Frauds with 21st Century Text Messages

In Massachusetts, the Statute of Frauds requires that contracts for the sale of real state must be in writing signed by the party (or agent) to be charged. In the old days of pen and paper, application of the Statute was quite simple. If there wasn’t a written agreement signed in wet, ink signatures, there was no binding contract. With the proliferation of e-mail and text communication, application of the Statute of Frauds has become much more nuanced.

In the case discussed here, Judge Robert Foster noted several recent judicial decisions holding that emails may be binding as well as the Uniform Electronic Transactions Act, under which parties may impliedly consent through their actions to make email and text transmissions binding and enforceable. Emphasizing the fact that the seller’s agent signed his name “Tim” at the end of the critical text message, the judge found that the text message was sufficiently “signed” under the Statute of Frauds to constitute a binding agreement at the culmination of the previous communications and unsigned letters of intent. The judge also found persuasive that the seller’s agent told the buyer’s agent to have the buyer sign the letter of intent first, and that’s exactly what the buyer did. Finding in favor of the buyer, the judge denied the seller’s motion to dismiss and issued a restraining order against the seller’s conveyance of the subject property.

Take Away: IMO, Watch What You Say!

This area of the law is really becoming a dangerous minefield. After the e-mail ruling came out a few years ago, I advised my clients to use the following disclaimer: “Emails sent or received shall neither constitute acceptance of conducting transactions via electronic means nor shall create a binding contract in the absence of a fully signed written agreement.”

The problem, however, with text messages is that they are so short and informal. It’s not practical to use a legal disclaimer on texts, and there’s no technology that I’m aware of that would insert one into every text. You could always start off a negotiation with the caveat that electronic communications will not create a binding contract until a formal offer is executed. Also, it’s always a good idea to end every email/text with “subject to seller/buyer review and approval” when negotiating an offer. But, such boilerplate language can always be waived by subsequent conduct or actions.

This case reminds me of Lomasney’s First Rule of Politics: “Never write if you can speak; never speak if you can nod; never nod if you can wink.” — and by winking that does not mean an emoji. ?

And always take screenshots of important texts…just in case.

This post is sponsored by Brian Cavanaugh, Senior Mortgage Banker, Mortgage Network

Or Will Low Inventory Bring Rain Showers? | The Spring Market 2016 Expert Panel Report

Wow, what a difference a year makes! Last year we had one of the snowiest winters on record and a foot of snow on the ground. This year, we have 70 degree record temps with the Charles Esplanade filled with runners. The winter weather always affects the spring real estate market, and last year the market got started unusually late. So will this year’s warm winter usher in a hot real estate market? Or will the pesky low inventory rain on our parade?

To answer these questions, I’ve brought in a panel of top Realtors who will give you the report from the trenches, from the City to the ‘burbs. So without further ado, let’s hear from the experts.

The Sudbury & Wayland Real Estate markets are easing into the always anticipated “Spring market.” Like a slow motion game of Dominos, many soon-to-be sellers are waiting for a house they would potentially buy to come on the market before they commit to putting their own homes on. With that, inventory has been low, but is increasing at a steady pace now that it is March and Mother Nature doesn’t seem as eager to make a point as she did last winter. Buyers are actively looking and although not every Open House attendee is a serious buyer, the high numbers of attendees are typically a good indicator of an active market. 2016 is starting to form as a healthy Real Estate market. — Gabrielle Daniels Henken and Carole Daniels — Coldwell Banker, Sudbury. www.LiveInSudburyMA.com

In Cambridge and Somerville, we’re still dealing with the inventory shortage — I don’t think it would be hyperbole to call it a crisis — that we’ve had for the last several years. And although the mild weather has brought buyers out in full force already this year, the listings are just beginning to trickle on, so we’re seeing 9, 10, 20 parties competing for the same home. Hopefully it will be a bit less brutal as we get further into March, but for the foreseeable future, demand will continue to outpace supply here. Lara Gordon–Gibson Sotheby’s Cambridge. www.cambridgeville.com

Dear Sellers, please don’t wait until spring to list your house at the SAME time as everyone else! Inventory is historically low so list now while you can be a real stand out in the market. Chances are you will bear a higher price as well! The Metrowest market is a popular market that’s constantly strong and growing. Due to the fact that we have 3 major highways that touch Metrowest, it is a popular spot for commuters to Boston and Worcester alike. Metrowest real estate is also a great investment! Heidi Zizza, Broker/Owner, mdm Realty, Framingham, MA

High demand, low inventory and continued low rates create a healthy and fiesty market in MetroWest! Investors still have great opportunities with multi-family properties and first time buyers who didn’t take a break this winter were able to achieve their housing goals without busting their budgets. Glad to report that TRID was just a small bump in the road and had far less direct impact on the financing process than expected. Ali Corton, Real Estate Executives Boston West www.liveinframinghamma.com

At the risk of sounding like a broken record, in Winchester, Arlington, Stoneham, Melrose, and the surrounding towns, quality inventory is scarce, and when it hits the market it’s scooped up within days. Buyers must be crystal clear about what they want, and then develop the stamina of a marathoner. They must be willing to brave packed open houses, make rapid decisions about writing offers, endure having 1,2,3,4 great offers rejected before securing a property. Sellers with quality listings are being presented with 10,12,20 offers, all over asking, all waiving contingencies, all with heartfelt letters and photos from buyers who are pulling out all the stops to get a house. As agents in today’s market one of our most important roles is to support our clients, both buyers and sellers, to remain calm and focused during the frenzy of the market. Katherine Waters-Clark, Re/Max-Winchester-Arlington

I work primarily with buyers and in towns from Bolton, Westford to Shrewsbury and even as far as Gardner and Ashburnham, when a house comes on the market and is in good condition it is snapped up quickly with multiple offers. I have had clients submit written letters with their offers to try and help sway a seller to choose them. The rates are still low and the lack of inventory on the market is making a rather difficult market to guide buyers. First time home buyers are overwhelemed with the speed things have to be done to get their offer picked. Sellers are in a good place when it comes to selling a home in this Spring Market. I just did an Open House in Metheun yesterday, I had 16 families come through and today our seller has 3 offers to choose from, this is going to be a great Spring Market. Sherry Stone-Graham,www.baystate-homes.com

The condo market in Metrowest is starving for inventory. I received 8 offers on one unit on Spyglass Hill in Ashland and a couple on a garden style unit. My open houses on Spyglass Hill have had over 25 guests. We desperately need inventory. So many buyers with so few properties is allowing sellers to possibly get more money. It’s a fantastic time to sell. Annie Silverman, Realty Executives Boston West.

I service Franklin and the surrounding area and am also licensed in RI. Right now the inventory is still low so sellers are really getting the activity they desire when priced correctly. My most recent listing had 23 sets of people through and we received 5 offers and most were over asking. Buyers are also fortunate as there was also just a dip in the financing rates. Franklin and most surrounding towns are also eligible for 0% down financing so the time is now to make the most of the Spring Market! Amber Cadaorette, Keller Williams Realty Franklin / Wrentham.ambersoldmyhouse.com

Feel free to offer your comments here or on Facebook! And good luck with your listings or buyers!

Scroll Down For My Complimentary TRID Rider and Offer Timeline Cheatsheet

I’ve been doing a lot of speaking, and more importantly, thinking and collaborating with loan officers and Realtors, on the impact of the new TRID (Truth in Lending RESPA/Integrated Disclosure) on Massachusetts residential real estate transactions. I know everyone is pretty much burned out with all this TRID talk, but what I will give you in this post is some hands-on, practical advice (like how to fill out an Offer) and forms to help you navigate TRID — best practices, if you will.

Those who are unfamiliar with TRID, the major change is that the Good Faith Estimate is going away in favor of a new “Loan Estimate” and the HUD-1 Settlement Statement is going away in favor of a new “Closing Disclosure.” TRID provides for specific deadlines as to when the Loan Estimate and Closing Disclosure must be delivered to the borrower. If those deadlines aren’t met, closings can be delayed for up to 7 days. For my comprehensive post on the new rules click here.

Change In Deadlines

The first major impact to real estate transactions will be the length of time to complete a transaction. The general consensus is that post-TRID, 60 day closings (from accepted offer) will be the norm. Will lenders be able to do 45 day closings? Yes, but only if all parties have their act together, and that’s a big “If.” Thirty (30) day closings will be nearly impossible to achieve, in my opinion.

So what does this mean? It means that all deadlines need to be tighter and that items typically left for the week or two prior to closing (like final readings and fuel adjustments) have to be done earlier in the transaction and closing table adjustments will be impossible.

Deadline to Submit Info For Closing Disclosure

One of the most important new dates will be the date on which all parties must provide the information necessary for the Closing Attorney and the lender to prepare the final Closing Disclosure (new HUD-1). TRID requires that the new Closing Disclosure issue to the borrower 3 days prior to closing (if sent electronically) or 7 days prior to closing (if sent by mail). Lenders will require all information necessary to prepare the CD well before this deadline. This will vary by lender anywhere from 10-20 days prior to closing. Also, some lenders intend to issue the Closing Disclosure along with the Loan Commitment. Accordingly, in my opinion the best practice under TRID is to target 20 days prior to closing by which all information needs to be submitted to the closing attorney. All parties should agree to this date in their purchase and sale agreements.

And by all information, what do I mean? See the graphic to the right.

Final Utility Readings and Oil/Fuel Adjustments

Although the TRID rules specifically allow for some last minute changes to the Closing Disclosure without triggering re-disclosure and delay in the closing, most of the lenders which I’ve consulted with do not intend to authorize last minute changes to the Closing Disclosure which might trigger a re-disclosure delay.

Given this, the Mass. Real Estate Bar Association (REBA) has proposed language in its new TRID rider that all utility readings (water, sewer, oil/fuel) be completed and submitted to the closing attorney no later than 10 days prior to closing. The Closing Disclosure shall reflect payment and adjustments as of the reading date except for real estate taxes which shall be adjusted as of the closing date. No further adjustments will be made on the Closing Disclosure, but the parties are free to make their own estimates of utilities as of the closing date.

This is a change to current practice where it’s common that the final readings be done a day or two prior to closing. I’ve spoken to several agents about oil fuel in particular, and they all say they really don’t want to deal with the hassle under TRID, so they will be recommending to their sellers that they simply gift the oil to the buyer.

Opt for Buyer Credits Instead of Seller Repairs

Seller repairs will cause major hassle and potential delays under TRID. Under TRID, all property repairs must be fully disclosed in the purchase and sale agreement and to the lender. No more “side agreements” or “repair agreements” outside the PS Agreement. Most lenders will require an inspection of all repairs prior to closing and some will do the inspection prior to the issuance of the Closing Disclosure. This would also necessitate a much earlier walk-through by the buyer to inspect those repairs. If there are problems with the repairs, or the insistence on a holdback which would be reflected on the Closing Disclosure, this could delay the issuance of the Closing Disclosure, and therefore delay the closing.

Accordingly, the general consensus is that it will be much cleaner under TRID to forgo seller repairs and instead have the seller agree to a closing cost credit to the buyer. This will eliminate the lender inspection, additional walkthrough and potential of delays.

Also, a quick word about holdbacks at closing. We are not sure how lenders will handle holdbacks at the closing but many of us are of the opinion that lenders will not allow a holdback unless it’s disclosed on the Closing Disclosure. So that effectively means no closing table holdback agreements unless you want your closing delayed to re-issue the Closing Disclosure.

Use a TRID Rider/Addendum for all Offers

MAR, GBREB and REBA have all come out with their own TRID riders. In my opinion, the MAR/GBREB riders don’t sufficiently protect buyers from delays and they fail to address utility/fuel adjustments. The REBA rider is better, but could still use some improvement. So naturally I’ve drafted my own rider (and TRID timeline cheatsheet) which is embedded below. Feel free to use it to help you fill out offers. Whatever rider/addendum you chose, just use something, otherwise your buyer will be at risk of losing their deposit over TRID delays.

Recommend Attorneys Who Specialize In Conveyancing/Closings

Residential real estate closing work was already complicated and highly regulated. In a TRID world, the pitfalls for the inexperienced and non-specialists will be myriad. Now more than ever, Realtors and loan officers should partner with experienced attorneys who specialize in residential closings and are TRID ready and compliant. Do not allow your clients to use their cousin who is a lawyer and knows very little about real estate. It could be disastrous for you and your transaction.

If you have any questions about TRID, Offers, Purchase and Sale Agreements, Riders, etc., please feel free to contact me at [email protected] or 508-620-5352. I would be happy to help you navigate the TRID maze.

Major Change To Current Practices | Expect Delays and Bumpy Road Starting Oct. 3

I just finished yet another closing where a national lender issued the closing documents the morning of the closing, and worse, issued a revised TIL (Truth in Lending) disclosure during the middle of the closing! Under the new TILA-RESPA Integrated Disclosure Rules (TRID) set to start on October 3, this too-common practice would have resulted in a closing delay of up to 7 days, to the dismay of everyone in the transaction.

The new TRID rules are game-changing regulations which threaten to disrupt and delay closings across the country. The new rules, already pushed back once due to industry outcry, go into effect in about 60 days on Oct. 3. I am very worried that lenders, Realtors and closing attorneys are not at all prepared for one of the most significant changes in how we do business. Experts are predicting that closings will be delayed, 60 day loan approvals will be the new normal, and new forms will bewilder buyers. “Expect a one- to two-week delay in closings,” said Ken Trepeta, director of real estate services of the government affairs branch for the National Association of Realtors, when describing the impact of TRID.

Currently, we are finishing one of the strongest spring markets in a decade, but I’m quite concerned that come Fall, the new TRID rules will put the fall market into an ice bath. The best thing that every real estate professional can do is get educated and get prepared now for these changes. August is typically a slow month, so use it to get ready. My team will be doing a roadshow Powerpoint seminar to any local real estate office to explain the new changes. Contact me at [email protected] for more info.

New Closing Disclosure Replacing the HUD-1 Settlement Statement: 3 Day Rule

Under TRID, there will be a new settlement statement called a Closing Disclosure, which must be issued to the borrower at least 3 days prior to closing. If that does not occur, the closing will be delayed for up to 7 days. We are hearing that lenders will require that the information contained in the Closing Disclosure (all fees, closing costs, taxes, insurance, escrows, credits, etc.) be finalized as early as 20 days prior to closing, to give them enough time to generate the new Closing Disclosure in a timely fashion and to account for delays.

What does that mean for us professionals? It means that everything will need to be pushed up and done faster than before. That goes for titles, CPL’s, broker commission statements, invoices for repairs, insurance binders, condo fees, recording fees, title insurance, everything. And it means we can all expect delays as everyone adjusts to the new timetables and rules.

Lenders will require the new Closing Disclosure (embedded below) be signed by the borrower at closing. However, although the Closing Disclosure was intended to replace the current HUD-1 Settlement Statement, the geniuses at CPFB neglected to put a signature line for the sellers on the new Closing Disclosure. I’m not making this up. And we are no longer supposed to use the “old” HUD-1 Settlement Statement. Thus, our title insurance companies are telling us that there may be three settlement statements signed at closing: a Closing Disclosure for the buyer, a Closing Disclosure for the seller, and a combined Closing Disclosure. ALTA has created a new Combined Settlement Statement which can be found here.

Bank of America was asked whether it would require the use of the ALTA model forms, and it stated in a June 9 memo that it prefers the ALTA model if a closing attorney chooses to use a settlement statement to supplement the Closing Disclosure (CD), but specified that the settlement statement figures must reconcile to the CD and a copy of the settlement statement must be provided to the bank. The bank also stated that all revisions to fees and costs will require bank approval and an amended CD. In other words, closing attorneys will not be allowed to revise fees and costs by simply supplementing the CD with a settlement statement.

60 Day Approvals/Closings The New Normal?

With any historic change to how lenders disclose fees and approve loans, there’s going to be a steep learning curve — and delays. You can count on that. Industry insiders say the days of 30 and even 45 day loan approvals may be over, at least temporarily. Sixty (60) day approvals may be the new normal, and agents should build the longer timeframe into their offers and purchase and sale agreements and educate their buyers and sellers accordingly.

Repairs and Walk-Throughs

Since lenders will require all fees and credits finalized 7-10 days prior to closing, this will significantly impact how we handle repairs and credits. Agreed upon repairs also affect how the appraisal is conducted which will further impact the timelines. Experts are suggesting that Realtors consider doing walk-throughs at least 14-21 days prior to closing instead of the typical day before or day of walkthrough, because all repair issues and credits should be set in stone at least 7-10 days prior to closing and changes in fees and credits on the day of closing will not be permitted by the lender. Some experts are even saying that agents should do two walkthroughs, one within the TRID timelines and one immediately prior to closing. Also, under TRID paid outside closing (POC) items will be discouraged by lenders.

Take-away: Realtors should be warned that repairs contained in the purchase and sale agreement will have the potential to delay closings under the TRID rules. Ensure that any repairs are completed 14-21 days prior to closing. Better yet, don’t have the seller make repairs at all; use closing cost credits instead.

No More Back to Back Closings?

Due to the high potential for delays caused by TRID, back-to-back or piggyback closings may be a thing of the past, at least for now. A delay with a closing obviously has a domino effect on a back to back closing. The best practice, at least for the first few months of the new TRID era, is to schedule closings at least 3 days apart. Seller/buyers will have to prepare for this reality with bridge loans, use and occupancy agreements, or temporarily staying with your nearest relatives.

Partner with Trusted and Verified Providers